You possess a business and so are pleased with your prosperity well-done! However when it comes time to make an application for a home loan, you will possibly not be because thrilled. Once the you are not brand new ‘typical W-2 wage earner,’ loan providers may not be since the amicable given that you’d guarantee. Your loan solutions rapidly dwindle, particularly if their taxation statements cannot tell you greatly income. As much as possible persuade Uncle sam that you do not generate far currency, most loan providers elizabeth.

Thank goodness, which is only for antique financial funding. Self-operating consumers for example yourself an unconventional financing. To put it differently, speaking of fund one to ‘think beyond your box’ plus don’t keep that such rigorous conditions. Solution loan alternatives assist consumers for example on your own pick its dream domestic even though you cannot verify your income the traditional method.

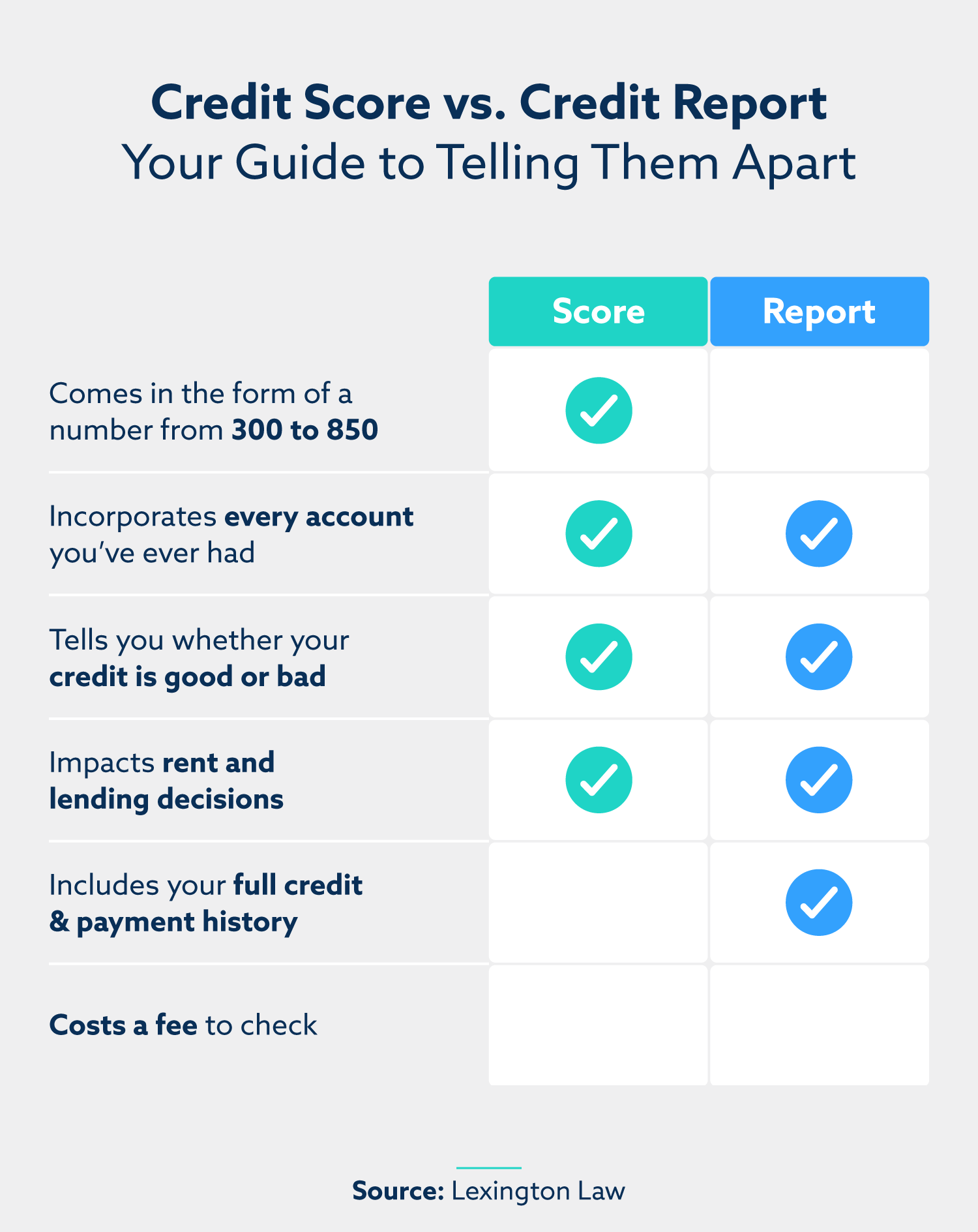

Exactly how Mortgages Benefit new Mind-Functioning

A mortgage is a home loan no matter where you performs. Lenders every have the same realization. They want to see you can afford the borrowed funds past a beneficial practical doubt. Antique and you can authorities-backed funds, not, enjoys stricter criteria. You need to prove your revenue the traditional way, and thus pay stubs, W-2s, and/or tax returns. If you are mind-employed even when, your age earnings just like the an excellent W-2 earner. The usa tax password lets entrepreneurs to enter away from a beneficial extreme percentage of their earnings. This is certainly great for the income tax liability however so good whenever lenders check your taxes and you may contour your income. It’s wise you to definitely thinking-working borrowers write off as much expenses as they possibly can. Who would like to spend much more fees than just called for? It generates a great organization sense, nevertheless you can expect to pose difficulty once you get an effective financial.

Right here is the disease. Loan providers utilize the exact same adjusted revenues which you allege into the the taxation. For many who individual a business and you may discount a section of your income, you appear ‘broke’ even though that is not happening. Conventional , FHA , USDA, and you can Va loan lenders need certainly to guarantee your income using your tax productivity. In case the taxation statements tell you absolutely nothing money, do you know what? From the vision of the lender, you will be making nothing money. One to simply leaves your instead of mortgage recognition. Having the current rules, loan providers need certainly to verify beyond a fair question that you could manage the borrowed funds. This won’t provide traditional or bodies-backed loan providers the capacity to undertake financial statements and other earnings paperwork to show you can afford the loan. Lenders has particular debt-to-income ratios you need to meet in order to qualify for the money. On the other hand, you must satisfy the income verification advice. Including delivering your tax returns to confirm their work.

The answer for Worry about-Employed Consumers: P&L Statement Finance and Bank Statement Finance

Yet, it does not voice promising getting mind-operating borrowers, proper? You’ll often keeps a hard time qualifying with your ‘lower income’ because of your income tax build-offs or you can easily pay a much higher price than just anticipated Kentucky loans since the of one’s chance your loan poses. If you need a home loan that does not penalize both you and helps make it easy so you can meet the requirements once the a personal-working borrower, thought applying for a P&L Report Loan otherwise a bank Statement Loan . Speaking of higher selection so you’re able to a vintage mortgage while they you should never manage the tax statements, however, make it other ways of earnings confirmation.

How P&L Report Mortgage loans Work

Mortgage individuals looking for a good subprime financing can apply toward P&L mortgage that’s one of the safest fund to possess thinking-functioning consumers to utilize. Instead of using your tax returns, you could potentially qualify to your last several years’ Earnings & Losings statements made by the accountant. The newest P&L informs us how much cash your bring in and you will just what you really can afford. We examine your income on the current costs because reported into your credit history as well as your credit score.